For buyers with a real deal on the table

Will the SBA Fund This Deal?

Know your walk-away price — and whether the deal clears the checks lenders actually run — before you sign the LOI.

Every rule verified against the current SBA SOP 50 10 8. And we don't sell your lead.

Get the Kit →Founding price: $67 Personal / $197 Professional · instant download

Most buyers find out a deal isn't fundable months in — from the lender who declines it. The rules that decide it are public (equity injection, collateral, coverage, seller structure), but they live in a 400-page SOP, and the free calculators that claim to check them exist to sell your contact information to lenders. The kit runs the whole underwrite yourself, on your numbers, in an afternoon.

Written by Thomas Hartwell, author of the FUNDED series of industry-specific SBA lending guides.

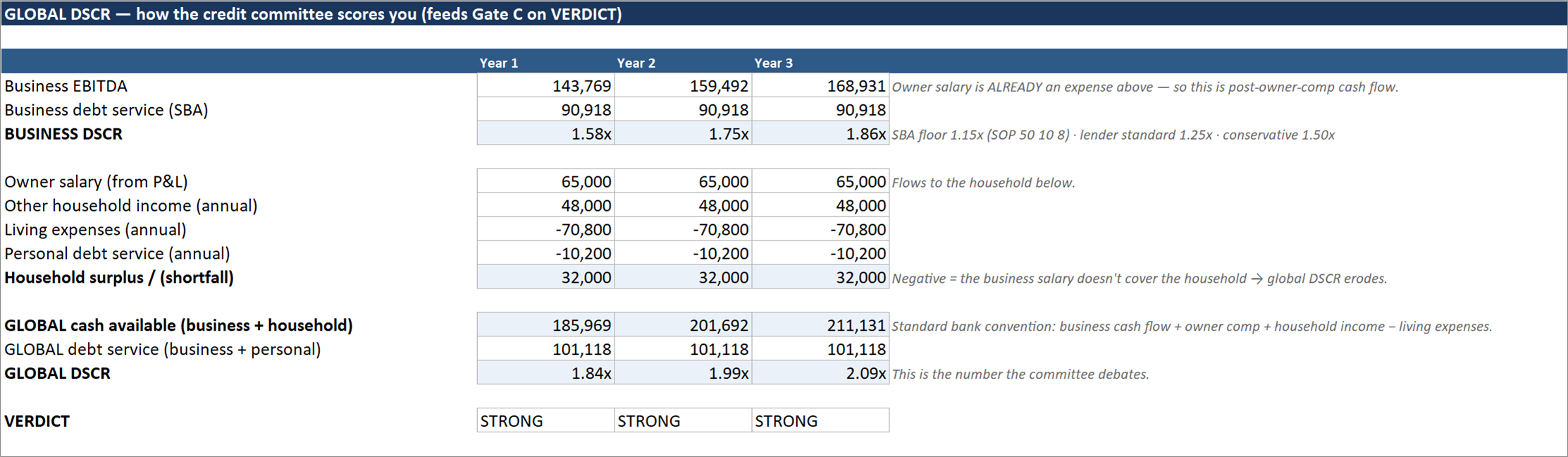

Three answers, on the front tab

Fill in the deal you're looking at. The workbook returns the three verdicts that decide whether to proceed.

1. Your walk-away price

The highest price at which the deal still covers its debt at the 1.25x coverage lenders want. "Above $X, walk away." Know your ceiling before the negotiation, not after the decline.

2. The financeability verdict

A PASS / RISK / FAIL panel on the three gates underwriters test: equity injection (the 10% floor, what counts, the seller-note standby rules), collateral adequacy (at the SOP's own valuation discounts), and global DSCR — including your household, the way banks actually compute it.

3. The red-flag score

Your deal scored against the structural killers: dirty add-backs that won't survive IRS-transcript verification, an earnout in the LOI (prohibited), a seller who isn't fully exiting, price above what a valuation will support, and more — each mapped to the SOP rule it violates.

See inside — the actual workbook

Unretouched screenshots from the restaurant edition, running the same sample deal you can download free below.

Built for the owner-operator, not the fund

The headline number is take-home cash after debt service — what's actually left for you each year after the loan payment — because that's the number you'll live on. Five-year projections are built on your industry's real operating benchmarks, with every formula open and defensible in a lender meeting.

(There's an investor-view tab with IRR and return math for partners who ask — but it's the second tab, not the pitch.)

What's in the kit

The deal-analysis workbook (Excel)

The core: walk-away price, financeability panel, red-flag score, five-year industry projections, take-home cash, DSCR at every threshold with the 10% stress test, and the investor-view tab. Formulas open, protection on the structure only.

Lender-ready business plan template (Word)

Structured the way loan files are read — the narrative sections underwriters expect, keyed to the workbook's numbers so the plan and the projections tell the same story.

Loan file tracker (Excel)

Every document the lender will ask for — Forms 1919 and 413, tax returns, interim financials, purchase agreement, valuation, insurance — tracked from "requested" to "in the file."

AI prompt pack + DSCR self-check mini

Prompts for using AI on diligence and plan drafting without inventing numbers, plus the standalone DSCR self-check spreadsheet for the quick first pass.

Five industry editions: Restaurant · Hotel · Franchise · Dental · Veterinary — pick yours at checkout.

The spec, exactly

- Version 1.0 · rules verified against SBA SOP 50 10 8 (effective June 1, 2025), 13 CFR Part 120, and FY2026 fee notices — as of July 2026

- Workbook (16 tabs): START · VERDICT · Deal Inputs · Sources & Uses · Debt Schedule · Revenue Build · P&L · Cash Flow · Balance Sheet · Personal Budget · Global DSCR · Deal Analyzer · Red Flags · Investor View · Benchmarks · License

- Formats: Excel (.xlsx, desktop or Microsoft 365) · Word (.docx) · plain-text prompt pack — 5 files, instant download

- Projections: monthly for 24 months + annual Years 1–5, the package format SBA lenders ask for

- Updates: free replacement files when SBA rules change, for as long as we publish the kit

Verified against the current rules

Every gate the kit tests is verified against the current SBA SOP 50 10 8 (effective June 1, 2025), 13 CFR Part 120, and the latest Procedural Notices — the same verification system behind the FUNDED book series. Buyers receive updates when the rules change. Most SBA content online still cites superseded SOPs; the 2025 SOP changed the injection and seller-note rules that decide deals.

We don't sell your lead

The free "SBA calculators" you'll find elsewhere are lender lead-generation — the product is your phone number. Hartwell Labs sells books and tools. Your deal information never leaves your spreadsheet, and your email is never sold or passed to a lender. That's the business model, in writing.

Two licenses

PERSONAL

$97

one-time

- ✓ Your own deals — as many as you like, forever

- ✓ All kit files for your industry edition

- ✓ Share your outputs with your lender, CPA, attorney

- ✓ Rule-change updates included

- ✓ 14-day refund window

PROFESSIONAL

$247

one-time · one named professional

- ✓ Everything in Personal

- ✓ Use with unlimited clients and borrowers

- ✓ Single-office internal training

- ✓ For lenders, brokers, consultants, CPAs, advisors

- ✓ 14-day refund window

Every delivered copy is stamped with the purchaser's email. Full license terms travel with the files. Same files in both tiers — the license, not the product, is the difference.

Educational tool — not financial, legal, tax, or lending advice, and not a guarantee of loan approval; lender and SBA decisions are made independently. Hartwell Labs LLC is not affiliated with, endorsed by, or sponsored by the U.S. Small Business Administration. Full disclaimer.

What the alternatives cost

Done-for-you SBA projections run $750–$3,500 from modeling shops, and an advisor's deal review starts around $500 — for one deal, without the rules. The kit is the same underwrite, self-serve, for every deal you ever look at.

The 14-day "it does what this page says" guarantee

Open it, run your deal. If the kit doesn't do what this page describes, email [email protected] within 14 days and we refund you — no forms, no "exit interview," no partial credits.

Get the kit — founding price

Founding launch pricing — the price rises to $97 / $247 after launch.

2. Choose your license

PERSONAL

$97 $67

your own deals, forever

Buy Personal →PROFESSIONAL

$247 $197

unlimited client use

Buy Professional →Instant download · secure checkout by Stripe · 14-day guarantee · we don't sell your lead.

Frequently Asked Questions

What does "Will the SBA fund this deal?" actually check?

The kit runs your deal through the same gates a lender's underwriter applies: the equity-injection requirement (SBA requires at least 10% of total project costs on a complete change of ownership, and a seller note only counts if it's on full standby and no more than half the injection), collateral adequacy using the SOP's own valuation discounts, and global debt-service coverage — the business's cash flow plus your household income against all business and personal debt. It also scores the deal against the red flags that kill applications, like earnouts in the LOI (prohibited when the buyer uses SBA financing) or books that won't reconcile to IRS transcripts.

What is a walk-away price?

The highest price at which the deal still covers its debt at the coverage level lenders want (1.25x). Above that number, the loan payment eats the cash flow and the deal stops being fundable — no matter how much you like the business. The kit computes it from the business's actual cash flow and puts it on the front tab, so you know your ceiling before you negotiate.

How is this different from the free calculators everywhere else?

Two ways. First, most free SBA calculators exist to capture and sell your contact information to lenders — we don't sell your lead, period. Second, free calculators check one number in isolation. The kit is the whole underwrite: five-year projections built for your industry, the financeability gates, the red-flag scan, the document tracker, and a lender-ready business plan template — with the formulas open so you can see and defend every number.

Which industries are covered?

Five editions, matched to the FUNDED book series: restaurant, hotel, franchise, dental practice, and veterinary practice. Each edition's projection model, benchmarks, and red flags are specific to that industry — a hotel deal is tested against occupancy and ADR logic, a franchise deal against royalty and fee loads, a practice deal against production and staffing norms.

What's the difference between the Personal and Professional licenses?

Personal ($97) covers your own deals — as many of your own transactions as you like, forever, including sharing your completed outputs with your lender, CPA, or attorney. Professional ($247) is for one named professional — a lender, broker, consultant, CPA, or advisor — who works on other people's deals: unlimited client use plus single-office training. Every delivered copy is stamped with the purchaser's email.

Is the SBA content actually current?

Yes — that's the core of the product. Every rule the kit tests against is verified against the current SBA SOP 50 10 8 (effective June 1, 2025), 13 CFR Part 120, and the latest Procedural Notices, and buyers receive updates when the rules change. Most SBA content online still cites superseded SOPs.

What if it doesn't fit my deal?

There's a 14-day refund window. If the kit doesn't do what this page says, write to [email protected] and we'll refund you.

I'm not an Excel person — can I actually use this?

Yes. You only ever type in the blue cells — plain-English inputs like the asking price, the rent, and your household budget. Every formula is pre-built and locked against accidents, each input has a note explaining where to find the number (the FDD item, the POS report, the lease), and the VERDICT tab turns it all into PASS/RISK/FAIL. If you can fill in a form, you can run the kit.

What do I need to run it? Does it work in Google Sheets?

Microsoft Excel — desktop or Microsoft 365 — on Windows or Mac. The workbooks use protected formulas and conditional formatting that Google Sheets doesn't fully support, so we don't recommend Sheets. The business plan template is a Word file; the AI prompt pack is plain text and works anywhere.

Is this a subscription?

No. One payment, yours forever — including the free updated files we send when SBA rules change. There is nothing recurring to cancel.

What support do I get?

Email support at [email protected] for anything about using the kit — a cell that confuses you, a number you can't find, a gate verdict you want to sanity-check. What we can't do is give financial, legal, or lending advice about your specific deal — the kit shows you the rules; your CPA and attorney advise you.